OTC Markets OTC Pink Current Reports – Material Corporate Events

In addition to the OTC Markets requirement that public companies on the OTC Pink Market file annual and quarterly reports, all companies on the OTC Pink Market are required to promptly disclose to the public any news or information regarding matters that may be material to the issuer and its securities even if that information is negative.

Persons with knowledge of such material events are considered to be in possession of material nonpublic information and may not buy or sell the issuer’s securities until or unless such information is made public.

If not included in the issuer’s previous OTC Markets filings and disclosures, or if the material events occur after the publication of such OTC Markets disclosures, the public company must publicly disclose such events by disseminating a news release within four (4) business days following their occurrence and posting such news release through an Integrated Newswire or the OTC Disclosure & News Service. Read More

Roadmap for a Successful Direct Public Offering

Preparing for a direct public offering or an initial public offering (“IPO”) or takes both a commitment of time and money. Unlike an Initial Public Offering, a direct public offering does not involve an underwriter. While it often takes a year or longer to plan for and complete an IPO, a direct public offering can be completed in as little as 90 days, using Form S-1. Unlike a Form 10 registration statement, Form S-1 will create unrestricted securities.

Money and time are not the only things required for a successful direct public offering. Having the right Going Public Attorney is critical to the direct public offering process. Some companies begin planning for their direct public offering months before the process begins. This allows the issuer to consider a variety of factors including confidential submission of the registration statement and other matters. During this time, the company prepares for the audit process, develops its plan of operations and obtains its shareholder base. Read More

Going Public and Direct Public Offerings Provide Benefits in 2025

Going public is still considered a benefit to issuers seeking to raise capital or obtain recognition of their business. Even in a down economy, private companies seek the perceived benefits of being publicly traded. While there are a variety of ways to create a publicly traded company, each comes with its own unique requirements and risks. The Direct Public Offering (“DPO”) eliminates many of the risks and expenses associated with reverse mergers into public shell companies. Issuers going public using a DPO also have fewer hurdles to obtaining electronic trading from Depository Trust Company (“DTC”).

Reverse merger companies often encounter DTC chills and global locks because of prior unregistered securities issuances and being public shells under prior management.

Types of Registered Offerings: Issuers going public with an Initial Public Offering (“IPO”) or DPO must file a registration statement pursuant to the Securities Act of 1933, as amended (the “Securities Act”). The most commonly used registration statement is Form S-1 for domestic issuers and Form F-1 for foreign issuers seeking to go public. Read More

Whistleblower Frequently Asked Questions

The SEC’s whistleblower program was established by Congress to incentivize whistleblowers to report specific, timely and credible information about possible federal securities laws violations.

The Commission is authorized to provide monetary awards to eligible individuals who come forward with high-quality original information that leads to an SEC enforcement action in which over $1 million in sanctions is ordered. The range for awards is between 10% and 30% of the money collected.

Since the whistleblower program’s inception in 2011, the SEC has awarded more than $2.2 billion to 444 individual whistleblowers. In 2024, the SEC awarded over $255 million to 47 whistleblowers. This was the third-highest annual amount awarded since the program began in 2011. Read More

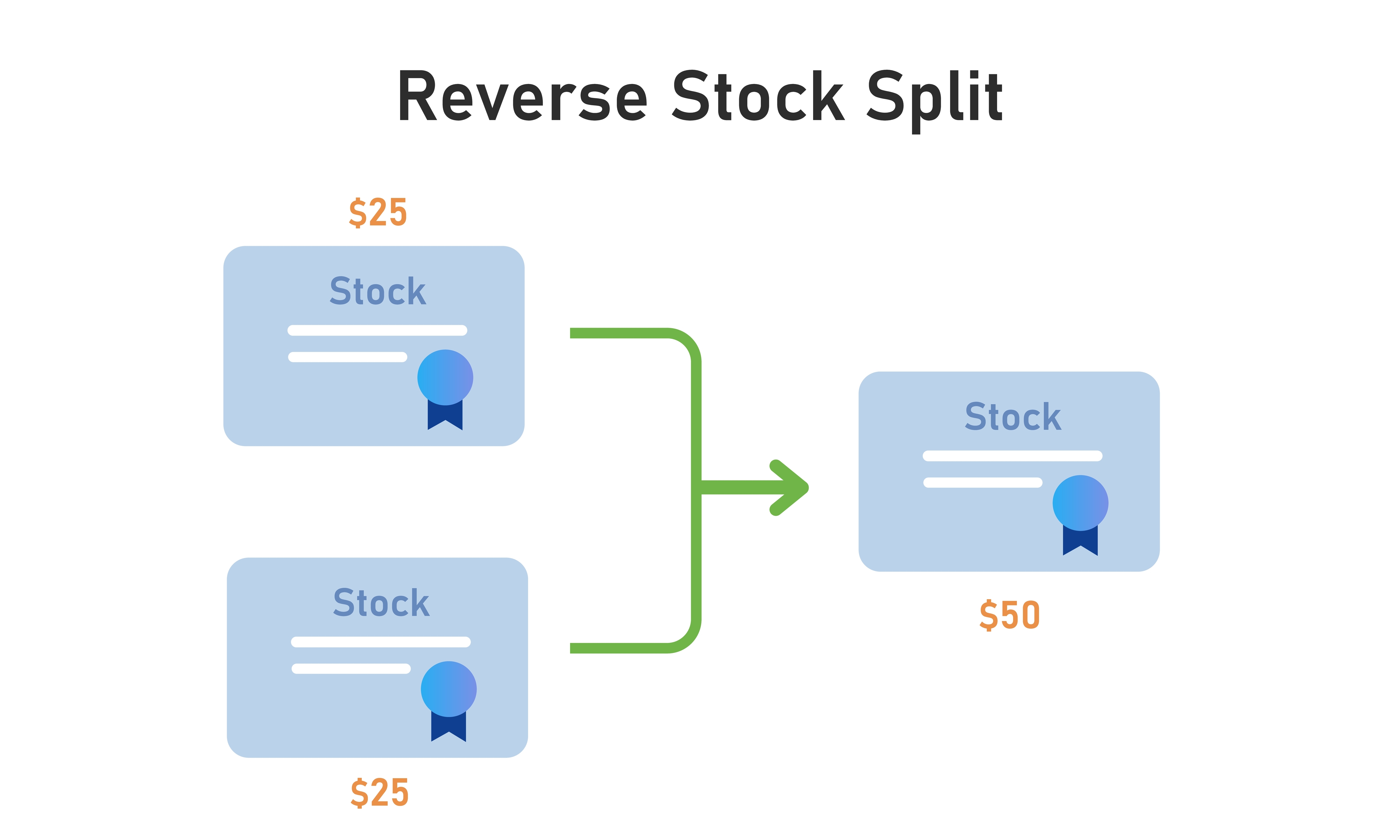

Reverse Stock Splits by Nasdaq and NYSE Issuers

Public Companies whose securities are listed on the New York Stock Exchange (NYSE) and Nasdaq Stock Market (NASDAQ), particularly the NASDAQ Capital Market, frequently effect reverse stock splits to comply with NASDAQ and NYSE’s minimum $1.00 share price requirement.

Reverse splits are neutral in theory. They only change the number of shares outstanding, not the value of shareholders’ positions in those shares. Therefore, they almost always increase the price of a public company’s securities by combining the issuer’s outstanding securities at a ratio so that after the reverse stock split, each stockholder maintains its approximate ownership percentage while the company has a lesser number of securities outstanding with a higher price per share.

However, it has become more common in recent years for exchange-listed companies (especially startups and biotechs) to enter into dilutive financings, where financiers receive securities in exchange for cash at a discount to the market price through convertible debt notes, convertible preferred stock, and warrants, which have a dilutive effect when converted/exercised, causing the company’s stock price to drop over time and leading to the company having to effect a reverse split to remain compliant with the listing standards. Oftentimes, companies involved in dilutive financings become repeat offenders, having to do two or more reverse splits to remain compliant with the listing standards. We’ve even witnessed some public companies effecting as many as four to five reverse stock splits in less than two years.

To address this issue, the NYSE and Nasdaq each proposed rule changes to limit a public company’s ability to enact a reverse stock split to regain compliance with the minimum share price requirement of $1.00 per share. Read More

SEC Settles with Morningview Financial, LLC and Its Managing Member, Miles M. Riccio, Alleged to Have Acted as Unregistered Dealers

On December 23, 2024, the United States District Court for the Southern District of New York entered final judgments on consent against Defendant Morningview Financial, LLC, a company alleged to have acted as an unregistered dealer; Defendant Miles M. Riccio, Morningview Financial’s managing member and partial owner; and Relief Defendant Joseph M. Riccio, Morningview Financial’s other partial owner who also received a portion of the alleged ill-gotten gains.

The SEC’s complaint, filed on September 23, 2022, alleged that Morningview Financial and Miles Riccio acted as securities dealers from approximately July 2017 through at least December 2021, notwithstanding the fact that they were not registered as dealers with the SEC, nor was Miles Riccio associated with an SEC-registered dealer. The SEC also alleged that Defendants funded 35 penny stock issuers in exchange for at least 68 convertible notes and 4 warrant agreements, converted the notes and the warrants to obtain more than 3.2 billion shares of newly issued shares of common stock, and then publicly sold over 90% of these new shares of common stock, generating over $14.8 million in trading profits. Read More

Pink Current will become OTCID on July 1, 2025

Over the past 25 years, the OTC Markets Group (OTCQX: OTCM) has made many changes to modernize the OTC Markets platform. This platform facilitates trading in over 12,000 securities, totaling hundreds of billions of dollars in transactions each year. One significant change was the introduction of the OTCQX and OTCQB markets, which hold companies to higher financial and disclosure standards.

In July 2025, OTC Markets Group will make another change: replacing Pink Current with OTCID. OTCID will be a Basic Reporting Market for companies that meet a minimal current information standard and provide management certification without the qualitative standards of our OTCQX and OTCQB markets.

Issuers that do not provide updated information, ongoing reporting, and the required management certifications will see their securities transition to the Pink Limited Market or the Expert Restricted Market, whichever is applicable. Read More

What Are American Depositary Receipts (“ADRs”)?

Many foreign companies use American Depositary Receipts (“ADRs”) as a means of going public to raise capital or establish a trading presence in the United States. ADRs are traded on exchanges like NASDAQ or NYSE as well as the OTC Markets.

An ADR is a negotiable certificate that evidences ownership of American Depositary Shares (“ADSs”), which, in turn, represent an interest in a specified number (or fraction) of a foreign company’s shares. The use of a ratio allows ADSs to be priced at an amount more typical for the U.S. public markets. While an ADR is a physical certificate evidencing an ADS, market participants often use the terms ADR and ADS interchangeably. ADRs trade in U.S. dollars and clear through U.S. settlement systems, allowing ADR holders to avoid effecting transactions in a foreign currency. Read More

Philip Verges Indicted for Manipulating Five Publicly Traded Companies and Defrauding Investors of Over $200M

On December 10, 2024, a federal grand jury in Dallas, Texas, returned an indictment charging a Texas businessman for his role in a yearslong scheme involving at least five publicly traded companies.

According to court documents, Philip Verges, 59, of Dallas, controlled five publicly traded companies, which he used to engage in an investment fraud scheme from approximately January 2017 through August 2022.

- Altemet Systems Inc. (“AL YI”) was a Wyoming corporation, with its principal place of business in Addison, Texas, which traded under the symbol ALYI

- Priority Aviation, Inc. (“PJET”) was a Wyoming corporation, with its principal place of business in Dallas, Texas, which traded under the symbol PJET

- Puration, Inc. (“PURA”) was a Wyoming corporation, with its principal place of business in Farmersville, Texas, which traded under the symbol PURA

- Vaycaychella, Inc. (“VAYK”) was a Wyoming corporation, with its principal place of business in Las Vegas, Nevada, which traded under the symbol VAYK

- Waterpure International, Inc. (“WPUR”) was a Florida corporation, with its principal place of business in Dallas, Texas, which traded under the symbol WPUR

Foreign Private Issuer Periodic Reporting on Form 20-F and Form 6-K

After a foreign private issuer has completed its going public transaction by completing an offering registered under the Securities Act of 1933, as amended (the “Securities Act”) or registered as a class of securities under the Exchange Act of 1934 (the “Exchange Act”), it is required as an SEC reporting company to file reports with the Securities and Exchange Commission (“SEC”) on an ongoing or continuous basis. Foreign Private Issuer SEC reporting requirements with the SEC are as follows: Read More

Clinton Greyling Sentenced for Role in Unregistered Broker Scheme

On December 11, 2024, Clinton Greyling, 50, of Tamarac, Fla., was sentenced by U.S. District Court Judge Richard G. Stearns to one year of probation. He was also ordered to perform 200 hours of community service and to forfeit $229,576.

Greyling was charged on July 30, 2024 with one count of acting as an unregistered broker; aiding & abetting. Greyling agreed to waive the Indictment and plead guilty to one count of aiding & abetting an unregistered broker. As part of his plea agreement, Greyling also agreed to forfeit $628,610, but that sum was later reduced to $229,576. Read More

SEC says John Clayton, owner of Standard Registrar and Transfer Co, secretly acquired and dumped millions of shares of microcap stocks.

On December 11, 2024, the Securities and Exchange Commission (the “SEC“) filed a complaint in the United States District Court for the District of Utah charging five individuals and three entities for their roles in a fraudulent scheme to secretly acquire and dump into public securities markets millions of shares of microcap stocks.

Utah residents John S. Clayton, Daniel W. Jackson, Donald H. Perry, and Clark M. Mower, and Maryland resident Timothy J. Rieu, along with entities Standard Registrar and Transfer Co., Inc., Chesapeake Group, Inc., and First Equity Holdings Corp. were named as defendants who allegedly engaged in the scheme. Nine other entities are named as relief defendants for their alleged receipt of illicit proceeds of the fraudulent scheme.

According to the SEC Complaint, from at least 2014 to 2024, Clayton engaged in a securities fraud scheme to secretly amass and then illegally sell stock of small, publicly traded companies (the “Public Issuers”), including:

- Flexpoint Sensor Systems, Inc. (“Flexpoint”), which is quoted on OTC Link ATS under the symbol “FLXT.”

- ForeverGreen Worldwide Corp. (“ForeverGreen”), which was quoted on OTC Link ATS under the symbol “FVRG” and is now revoked.

- KwikClick, Inc. (“KwikClick”), which is quoted on OTC Link ATS under the symbol “KWIK.”

- LZG International Inc. (“LZG International”), which was quoted on OTC Link ATS under the symbol “LZGI.”

Clayton carried out his fraud, in part, through his companies, First Equity and Standard Registrar. Clayton was aided and abetted in his scheme by Jackson, Perry, Mower, Rieu, and Chesapeake. Read More

Court of Appeals partially Rules in Favor of Alpine Securities but Alpine not out of the woods yet

On November 22, 2024, the United States Court of Appeals for the District of Columbia Circuit in Washington, D.C., made its ruling in a case involving Alpine Securities Corporation (“Alpine”) and the Financial Industry Regulatory Authority (“FINRA“), reversing a decision by a lower court and siding, in part, with Alpine.

Alpine had brought a lawsuit against FINRA challenging FINRA’s constitutionality after FINRA initiated an expedited hearing to expel Alpine from the industry. Alpine sought a preliminary injunction from the district court against the expedited proceeding, arguing that FINRA is unconstitutional because its expedited action against Alpine violates either the private nondelegation doctrine or the Appointments Clause. The district court denied the preliminary injunction.

Alpine then appealed the district court’s decision to the United States Court of Appeals for the District of Columbia Circuit in Washington, D.C. In its Decision, the Court of Appeals reversed the district court’s decision to allow FINRA to expel Alpine without an SEC review saying that:

“FINRA may not expel Alpine either before Alpine has obtained full review by the SEC of the merits of any expulsion decision or before the period for Alpine to seek such review has elapsed.“

At the same time, the Court of Appeals declined to order the SEC not to expedite its own review, writing that:

“Alpine has not demonstrated that it will suffer irreparable harm from participating in the expedited proceeding itself as long as FINRA cannot expel Alpine until after the SEC conducts its own review. For that reason, Alpine has not shown that it is entitled to a preliminary injunction halting that proceeding altogether.“

For now, Alpine is in the clear and allowed to continue operating as a FINRA-member broker-dealer. But it’s not out of the woods yet. The Court of Appeals only ruled to allow Alpine to continue to operate pending a full review by the SEC, delaying its expulsion for the time being. Time will tell if Alpine can avoid expulsion altogether. Read More

What to Expect From Trump’s SEC

Market participants are speculating about the new Trump deregulation agenda and how it will impact the SEC. With Republicans in control of the 119th Congress, we expect to see SEC deregulation and changes aimed at capital formation and easing burdens on public companies. The incoming Trump administration will likely emphasize that reduced regulatory burdens may be beneficial to investments in new projects, expanded operations, and increased hiring. Of course, the existing regulatory scheme warns that deregulation would lead to excessive risk and lead to increased fraud.

Trump has been a strong supporter of digital assets and cryptocurrencies, which may result in scaling back enforcement actions as well as proposing new regulations or designating another enforcement agency to regulate this area, such as the the CFTC.

We also expect that controls and procedures violations will be reduced or eliminated and the SEC will scale back, eliminate, or not pursue enforcement actions for defective environmental, social, and corporate governance disclosures, absent an egregious fraud.

The SEC Announces Enforcement Results for Fiscal Year 2024

On November 22, 2024, the Securities and Exchange Commission announced that it filed 583 total enforcement actions in fiscal year 2024 while obtaining orders for $8.2 billion in financial remedies, the highest amount in SEC history.

The 583 enforcement actions represent a 26 percent decline in total enforcement actions compared to fiscal year 2023. Of those cases, the Commission filed 431 “stand-alone” actions, which was 14 percent less than in the prior fiscal year; 93 “follow-on” administrative proceedings seeking to bar or suspend individuals from certain functions in the securities markets based on criminal convictions, civil injunctions, or other orders, which was 43 percent less than the prior fiscal year; and 59 actions against issuers who were allegedly delinquent in making required filings with the SEC, which represented a decrease of 51 percent.

The $8.2 billion in financial remedies consisted of $6.1 billion in disgorgement and prejudgment interest, also the highest amount on record, and $2.1 billion in civil penalties, the second-highest amount on record. Approximately 56 percent of the $8.2 billion financial remedies ordered is attributable to a monetary judgment obtained following the SEC’s jury trial win against Terraform Labs and Do Kwon, who were charged with one of the largest securities frauds in U.S. history.

In addition, in fiscal year 2024, the SEC obtained orders barring 124 individuals from serving as officers and directors of public companies, the second-highest number of such bars obtained in a decade.

In fiscal year 2024, the SEC distributed $345 million to harmed investors, marking more than $2.7 billion returned to investors since the start of fiscal year 2021. The SEC also received 45,130 tips, complaints, and referrals in fiscal year 2024, the most ever received in one year, including more than 24,000 whistleblower tips, more than 14,000 of which were submitted by two individuals. The SEC issued whistleblower awards totaling $255 million. Read More

SEC brings charges against BIT Mining Ltd, Azure Power Global Ltd and Adani Green Energy Ltd in alleged massive bribery schemes

This week, the Securities and Exchange Commission (the “SEC“) brought charges in three separate alleged massive bribery schemes.

In action #1, brought on November 18, 2024, the SEC announced that BIT Mining Ltd., formerly known as 500.com Limited, agreed to pay a $4 million civil penalty to resolve charges that it violated the Foreign Corrupt Practices Act (FCPA) from 2017 to 2019 by engaging in a widespread bribery scheme to influence numerous foreign officials, including members of Japan’s parliament, in efforts to establish an integrated resort casino in Japan.

500.com was an online sports lottery service provider headquartered in Shenzhen, China, whose shares traded on the New York Stock Exchange (“NYSE”) under the symbol “WBAI.” In 2021, the issuer changed course and entered the cryptocurrency industry, changing its name and symbol to BIT Mining Ltd (BTCM). As of today, it trades on the NYSE.

The SEC’s order finds that the bribery scheme involved illicit payments of approximately $2.5 million in the form of cash bribes, entertainment, and extravagant trips. The order further finds that the bribes were authorized by a 500.com senior executive and that, after the bribery scheme came to light, the company never entered the market. Read More

The SEC’s Amended “Dealer” Definition for Toxic Lenders

In the past five years or so, we’ve written many times about “toxic lenders”. These toxic lenders have been active since the end of the last century and have flourished providing financing to small publicly traded companies quoted by the OTC Markets. The kind of financing they offer is called “market adjustable” by the Securities and Exchange Commission and “toxic funding” or “death spiral funding” by many of its victims. The way it works is simple: the financier and the public company sign agreements binding each party to certain obligations and guaranteeing each party certain rights.

The public company will usually get money upfront. In return, the public company will issue market adjustable securities—a promissory note, preferred stock, warrants, debentures—to the toxic lender. The “market adjustable” part of the deal means that the securities sold will be convertible to common stock at a price that adjusts based on the public company’s trading price. Sometimes, the shares are registered with the SEC and can be sold immediately, and other times, the toxic lender can’t sell immediately because the convertible instrument will be subject to Rule 144, which means a holding period applies. The lender can’t sell for six months if the public company is an SEC registrant, or one year if it is not.

In a perfect world, these kinds of loans would be a great success for all involved: the public company, a startup, or at least a young company, would get the cash it needs in the short term and can use it to make more money, with which it could pay off the loan. In the end, the deal would cost him only a reasonable amount of interest.

But the world is not perfect, and this kind of financing comes with a catch. There is some risk for the toxic lender, because the value of the stock in question may be lower, not higher, when they seek to sell from the time the stock purchase agreement is signed. To compensate for this risk, the toxic lender will receive a large discount to the market price of the stock when he does convert and sell. The discount is usually between 40 and 50 percent but may be as high as 60 or 70 percent.

SEC Charges Olayinka Oyebola and His Accounting Firm With Aiding and Abetting Massive TINGO Fraud

On September 30, 2024, the Securities and Exchange Commission (the “SEC“) charged Olayinka Oyebola and his Public Company Accounting Oversight Board-registered accounting firm, Olayinka Oyebola & Co. (Chartered Accountants), with aiding and abetting a massive securities fraud perpetrated by Mmobuosi Odogwu Banye, also known as Dozy Mmobuosi, and three related U.S. companies that Mmobuosi controlled (the Tingo entities).

On December 18, 2023, the SEC announced charges against Mmobuosi Odogwu Banye, a/k/a Dozy Mmobuosi, and three affiliated U.S.-based entities of which he is the CEO – Nasdaq-listed Tingo Group Inc., OTC-traded Agri-Fintech Holdings Inc. (fka Tingo Inc.), and Tingo International Holdings Inc. – in connection with an alleged multi-year scheme to inflate the financial performance metrics of these companies and key operating subsidiaries to defraud investors worldwide.

Securities Attorney Matthew C McMurdo suspended by the SEC

On September 20, 2024, the Securities and Exchange Commission (the “SEC” or “Commission”) issued an Administrative Order against securities attorney Matthew C. McMurdo for violating Section 4C of the Securities Exchange Act of 1934 (“Exchange Act”) and Rule 102(e)(1)(ii) of the Commission’s Rules of Practice.

According to the Order, from 2016 – 2021, McMurdo, who has been licensed to practice law in the state of New York since 1998, was engaged as corporate counsel for Enviro Impact Resources, Inc., f/k/a Industry Source Consulting, Inc. (“INSO”), is a non-SEC reporting, microcap public company with multiple former names, including Vega Biofuels, Inc. (“Vega”). During that time, McMurdo signed and then issued 10 opinion letters (“Opinion Letters”) addressed to OTC Markets, in which he opined on various annual and quarterly disclosure reports issued by Vega and INSO. Vega and INSO used these Opinion Letters to be quoted on OTC Markets and to allow broker-dealers to quote the stock of Vega and INSO. Read More

SEC Charges Multiple Individuals and Entities in Relationship Investment Scams

On September 17, 2024, the Securities and Exchange Commission (the “SEC“) charged five entities and three individuals in connection with two relationship investment scams involving fake crypto asset trading platforms NanoBit and CoinW6, respectively. The SEC’s two complaints allege that the schemers used WhatsApp, LinkedIn, and Instagram to gain the trust and confidence of the victims before luring them to fake crypto asset trading platforms and stealing their money. These charges are the SEC’s first enforcement actions alleging these types of scams.

Commissioner Mark Uyeda Dissents in Unregistered Dealer SEC Enforcement Action

Over the past few years, we have closely followed the Securities and Exchange Commission (the “SEC” or the “Commission”) as it has brought a parade of actions against lenders that purchase variable-rate convertible notes from public companies.

- 11/17/2017 – SEC v. Ibrahim Almagarby and Microcap Equity Group LLC (Complaint)

- 2/26/2020 – SEC v. John D Fierro and JDF Capital, Inc. (Complaint)

- 3/24/2020 – SEC v. Justin W. Keener D/B/A JMJ Financial (Complaint)

- 9/03/2020 – SEC v. John M. Fife, Chicago Venture Partners, L.P., Iliad Research and Trading, L.P., St. George Investments LLC, Tonaquint, Inc., and Typenex Co-Investment, LLC (Complaint)

- 8/13/2021 – SEC v. GPL Ventures, Alexander J. Dillon, Cosmin I. Panait, GPL Management LLC, et. al., (Complaint)

- 9/24/2021 – SEC v. Carebourn Capital, L.P. and Chip Alvin Rice (Complaint)

- 6/07/2022 – SEC v. LG Funding, LLC and Joseph Lerman (Complaint)

- 8/02/2022 – SEC v. Crownbridge Partners, LLC, Soheil Adhoot, and Sepas Ahdoot (Complaint)

- 9/22/2022 – SEC v. Morningview Financial, LLC and Miles M Riccio (Complaint)

- 6/01/2023 – SEC v. Auctus Fund Management, LLC, Louis Posner and Alfred Sollami, and Auctus Fund LLC (Complaint)

- 6/16/2023 – SEC v. BHP Capital NY, Inc. and Bryan Pantofel (Complaint)

- 9/28/2023 – SEC v. Adam Long, L2 Capital, LLC., and Oasis Capital, LLC (Complaint)

- 1/23/2024 – SEC v. Aryeh Goldstein, Adar Bays, LLC, and Adar Alef, LLC (Complaint)

- 4/29/2024 – SEC v. Tri-Bridge Ventures, LLC and John Francis Forsythe, III (Complaint)

- 5/7/2024 – SEC v. Curt Kramer, Power Up Lending Ltd., Geneva Roth Remark Holdings, Inc., and 1800 Diagonal Lending, LLC (formerly known as Sixth Street Lending LLC) (Complaint)

- 8/19/2024 – SEC v. GHS Investments, LLC, Mark S. Grober, Sarfraz S. Hajee, and Matthew L. Schissler (Administrative Proceeding)

In each of the above-listed cases, the SEC targeted the lender because they had engaged in the regular business of acquiring convertible, variable-rate notes from penny stock securities issuers, converting the notes into stock at a substantial discount from the prevailing market price, and selling the resulting newly issued shares of the issuers’ stock into the public market to obtain profits. Read More

Mullen Automotive (MULN): What to Do About Serial Reverse Splitters

At noon on September 13, 2024—Friday the 13th—Mullen Automotive (MULN) announced a 1:100 reverse stock split to become effective on September 17 at 12:01 a.m. The news did not come as a surprise to shareholders. MULN had held a Special [Stockholder] Meeting on September 9, 2024. The meeting, which was originally scheduled for September 13, was virtual. Its chief order of business was to vote on several issues. Votes from those not present had to be submitted electronically by 11:59 p.m. Pacific Standard Time on September 8. The company reports in its press release about the split that voting stockholders approved the split. And they did, by better than two to one. Of course, ballots not returned were presumably counted as votes in favor of the board’s proposals.

The press release also informs observers that “The Reverse Stock Split will not change the par value of the Common Stock nor the authorized number of shares of Common Stock, preferred stock or any series of preferred stock.” The company has 5 billion shares of common stock authorized. There are also three classes of preferred stock, warrants, and other convertible securities. Read More

SEC Charges Seven NASDAQ Listed Public Companies with Violations of Whistleblower Protection Rule

On September 9, 2024, the Securities and Exchange Commission (the “SEC”) announced settled charges against seven public companies for using employment, separation, and other agreements that violated rules prohibiting actions to impede whistleblowers from reporting potential misconduct to the SEC. To settle the SEC’s charges, the companies agreed to pay more than $3 million combined in civil penalties.

- Acadia Healthcare Company, Inc. (ACHC) agreed to pay a $1,386,000 civil penalty;

- a.k.a. Brands Holding Corp. (AKA) agreed to pay a $399,750 civil penalty;

- AppFolio, Inc. (APPF) agreed to pay a $692,250 civil penalty;

- IDEX Corporation (IEX) agreed to pay a $75,000 civil penalty;

- LSB Industries (LXU) agreed to pay a $156,000 civil penalty;

- Smart for Life, Inc. (SMFL) agreed to pay a $19,500 civil penalty; and

- TransUnion (TRU) agreed to pay a $312,000 civil penalty.

Are SEC Whistleblower Awards the Road to Riches or a Waste of Time?

On August 23, 2024, the Securities and Exchange Commission (“SEC”) announced It had awarded a total of $98 million to two SEC whistleblowers “whose information and assistance led to an SEC enforcement action and an action brought by another agency.” The first lucky tipster, whose contribution prompted the opening of an investigation and who provided continuing assistance, will pocket a cool $82 million. The second will receive $16 million.

In its press release about the awards, the SEC explained briefly how the program works:

Payments to whistleblowers are made out of an investor protection fund, established by Congress, which is financed entirely through monetary sanctions paid to the SEC by securities law violators. Whistleblowers may be eligible for an award when they voluntarily provide the SEC with original, timely, and credible information that leads to a successful enforcement action. Whistleblower awards can range from 10 to 30 percent of the money collected when the monetary sanctions exceed $1 million.

In the associated SEC Order, the circumstances surrounding the awards are explained fully, but not to us. The document is heavily redacted to protect the whistleblowers’ identities. We do learn that Claimant I alerted SEC staffers to the conduct that prompted the opening of an investigation and that he or she met with them “multiple times” and provided “additional helpful submissions.” Claimant II, apparently acting independently of Claimant I, offered “new helpful information” a year after the investigation had been opened, saving staff time and resources. Claimant I’s information addressed all the transactions in the covered actions filed by the SEC and the “other agency,” while Claimant II’s submission addressed only one of them. Read More

Court Vacates Order in Unregistered Dealer, Crown Bridge Partners Case

On August 19, 2024, the United States Court of Appeals for the Second District in New York ruled in the case of Darkpulse, Inc., Social Life Network, Inc. and Redhawk Holdings Corp. v. Crown Bridge Partners LLC and its managing members, Soheil Ahdoot and Sepas Ahdoot. The Plaintiffs were appealing the ruling of the United States District Court Southern District of New York, which dismissed the case on September 29, 2023. Read More

GHS Investments LLC and its owners, Mark Grober, Sarfraz Hajee and Matthew Schissler, settle with SEC – agree to pay disgorgement and fines and surrender remaining notes, warrants and stock.

On August 19, 2024, GHS Investments, LLC (“GHS”) and its owners, Mark Grober, Sarfraz Hajee and Matthew Schissler, came to a settlement with the Securities and Exchange Commission (the “SEC“), agreeing to pay disgorgement and fines and surrender remaining notes, warrants and stock.

According to the SEC, from 2017 through 2022 (the “relevant period”), GHS operated as an unregistered securities dealer and sold billions of shares of stock from at least 23 issuers into the public market and generated millions of dollars in profits for its own account. During the relevant period, GHS engaged in the regular business of acquiring convertible, variable rate notes from penny stock securities issuers, converting the notes into stock at a substantial discount from the prevailing market price, and selling the resulting newly issued shares of the issuers’ stock into the public market to obtain profits from the difference between the discounted share price it received and the prevailing market price of the stock.

Because GHS was not registered with the SEC as a securities dealer, GHS avoided certain regulatory obligations that govern the conduct of dealers in the marketplace, including the requirements to follow financial responsibility rules and maintain certain books and records. Grober, Hajee, and Schissler managed the day-to-day operations of GHS and shared the decision-making authority over GHS’s acquisition and disposition of convertible notes during the relevant period. As a result, GHS violated and Grober, Hajee, and Schissler caused GHS’s violations of Section 15(a)(1) of the Exchange Act.

GHS will pay $2,030,806 in disgorgement, prejudgment interest of $221,458.43, and a civil penalty of $173,080.62. Each of Grober, Hajee and Schissler will also pay a $10,000 penalty and consent to cease and desist from committing or causing any violations and any future violations of Section 15(a)(1) of the Exchange Act.

GHS will also have to (i) surrender for cancellation all rights to all shares of common stock that it received in connection with convertible, variable rate notes; (ii) surrender all conversion rights under all remaining convertible, variable rate notes; and (iii) surrender for cancellation and retirement all remaining warrants that it received in connection with convertible, variable rate notes. Read More

SEC Charges OTC Link LLC with Failing to File Suspicious Activity Reports

On August 12, 2024, the Securities and Exchange Commission (“SEC“) announced charges against OTC Link LLC, a New York-based broker-dealer, for failing to file numerous reports of suspicious financial transactions, known as Suspicious Activity Reports (SARs), for a period of more than three years. OTC Link agreed to pay $1.19 million to settle the charges.

To help detect potential securities law and money-laundering violations, broker-dealers like OTC Link are required to file SARs describing suspicious transactions conducted through their firms. According to the SEC’s order, OTC Link is an indirect, wholly-owned subsidiary of OTC Markets Group, Inc. It has been registered with the SEC as a broker-dealer since 2012. OTC Link’s sole line of business is its operation of three alternative trading system (ATS) platforms, OTC Link ATS, OTC Link ECN, and OTC Link NQB. The three OTC Link ATSs are used by broker-dealers on a daily basis to execute or facilitate tens of thousands of transactions in over-the-counter (OTC) securities, many of which are considered microcap or penny stock securities.

Cassava Sciences (SAVA) Faces an Indictment and at Least Two Investigations

Cassava Sciences (SAVA) is a Nasdaq issuer that claims to have developed a treatment for Alzheimer’s disease; the product is currently in Phase 3 trials. It’s called Simufilam, and the company says it not only stops the progression of the disease but also reverses its effects. In 2021, its stock spiked and sold off dramatically several times, though its price entered what would become an extended decline in the last months of the year. Read More

Meta Materials (MMAT) Declares Chapter 7 Bankruptcy

On Friday, August 9, 2024, Meta Materials Inc. (MMAT) filed for Chapter 7 bankruptcy. This turn of events was reported only in a Form 8-K filed with the SEC; no press release or announcement on the company website followed. The filing said simply:

Item 1.03. Bankruptcy or Receivership.

On August 9, 2024, after consideration of all strategic alternatives, Meta Materials, Inc., a Nevada corporation (the “Company”), ceased operations and filed a voluntary petition for relief under the provisions of Chapter 7 of Title 11 of the United States Code, 11 U.S.C. §101 et seq. (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Nevada (the “Bankruptcy Court”), Case No. 24-50792 (the “Bankruptcy Filing”).

As a result of the Bankruptcy Filing, a Chapter 7 trustee will be appointed by the Bankruptcy Court and will administer the Company’s bankruptcy estate, including liquidating the assets of the Company in accordance with the Bankruptcy Code. Once a Chapter 7 trustee is appointed, an initial hearing for creditors will be scheduled, and the Notice of Bankruptcy Case Filing will be sent to known creditors.

Item 5.02. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers.

On August 7, 2024, the Company terminated all of its remaining employees and executive officers, including Uzi Sasson, its President and Chief Executive Officer, and Dan Eaton, its Chief Legal Officer, with the terminations of Messrs. Sasson and Eaton effective concurrent with the Bankruptcy Filing. Following the Bankruptcy Filing, the Company does not have any executive officers or employees.

Effective concurrent with the Bankruptcy Filing, each of John R. Harding, Allison Christilaw, Steen Karsbo, Kenneth Hannah, Vyomesh Joshi and Philippe Morali tendered their resignations as members of the Board of Directors. Each of the directors resigned due to the Bankruptcy Filing, and such resignations are not the result of any disagreements with the Company regarding the Company’s operations, policies, or practices. The resignation of the Company’s directors effectively eliminates the powers of the Board of Directors, and following the director resignations, the Company does not have directors serving on the Board of Directors.

The Chapter 7 filing has yet to turn up at the U.S. Bankruptcy Court for the District of Nevada, but it will be available soon. A trustee will be appointed, and he or she will handle the liquidation of the company’s assets. Read More

SEC Charges Ideanomics, its former Chairman and CEO, Zheng (Bruno) Wu, current CEO, Alfred Poor, and former CFO, Federico Tovar with Accounting and Disclosure Fraud

On August 9, 2024, the Securities and Exchange Commission (“SEC“) announced settled fraud charges against Ideanomics, Inc., formerly known as Seven Stars Cloud Group, Inc., and its former Chairman and CEO, Zheng (Bruno) Wu, for misleading the public about the company’s financial performance between 2017 and 2019. The SEC also announced settled charges against Ideanomics’ current CEO, Alfred Poor, and former CFO, Federico Tovar, for their roles in the scheme. Read More