offering, which allows you to raise an unlimited amount, might be the appropriate choice.")

Crowdfunding Offerings in the Time of Coronavirus

In the past few months, the COVID-19 outbreak has caused quarantines and closures, and has restricted the movement of people and goods between countries and within the United States. It has devastated certain industries and economies at home and abroad. Uncertainty about the duration of the crisis has roiled the financial markets, leading to worries about a global recession to come. Large businesses like Boeing will survive, as in 2008, because they’re “too big to fail,” but the small businesses that are the real backbone of the U.S. economy may face hardship. Some—the lucky ones—will need to raise capital to respond to increased demand for their crisis-related products; others will need additional cash to keep their businesses viable during the pandemic.

U.S. small businesses are left unsure whether they’ll survive without an injection of cash. While government relief is in the works, many businesses won’t qualify, or the resources available to them will not be enough to address their needs. But some industries will not be impacted, and may even experience growth during the coronavirus crisis. Companies in these industries that need capital to meet rising demand should consider crowdfunding a securities offering as an option.

According to BackerKit, a firm that says it “helps crowdfunding backers and creators, connect, support each other, and get the most out of every campaign,” reports that in the past two weeks they’ve been told by creators that despite the outbreak, backers haven’t lost interest in their projects. Tabletop Games and Barrel Aged Games recently launched Kickstarter crowdfunding campaigns that met their goals on the first day.

Small companies with suitable products or services—ones that will continue to be in demand as the crisis continues—should make an educated determination of whether crowdfunding a securities offering is a viable option for them at this time. Companies already conducting crowdfunding offerings should consider disclosure obligations they may have due to the COVID-19 outbreak.

This month, our firm will be releasing a book called Crowdfunding Guide, written by Brenda Hamilton and her colleague Michael Williams, who is also a securities attorney. Its purpose is to educate and inform small business owners about the opportunities created by the various exempt offerings involving crowdfunding created by the Securities and Exchange Commission.

In this blog post, we discuss choosing the right crowdfunding exemption for your securities offering. Over the next two weeks, we will be doing a series of short articles discussing the benefits and requirements of each crowdfunding exemption.

Crowdfunding Exemptions from SEC Registration

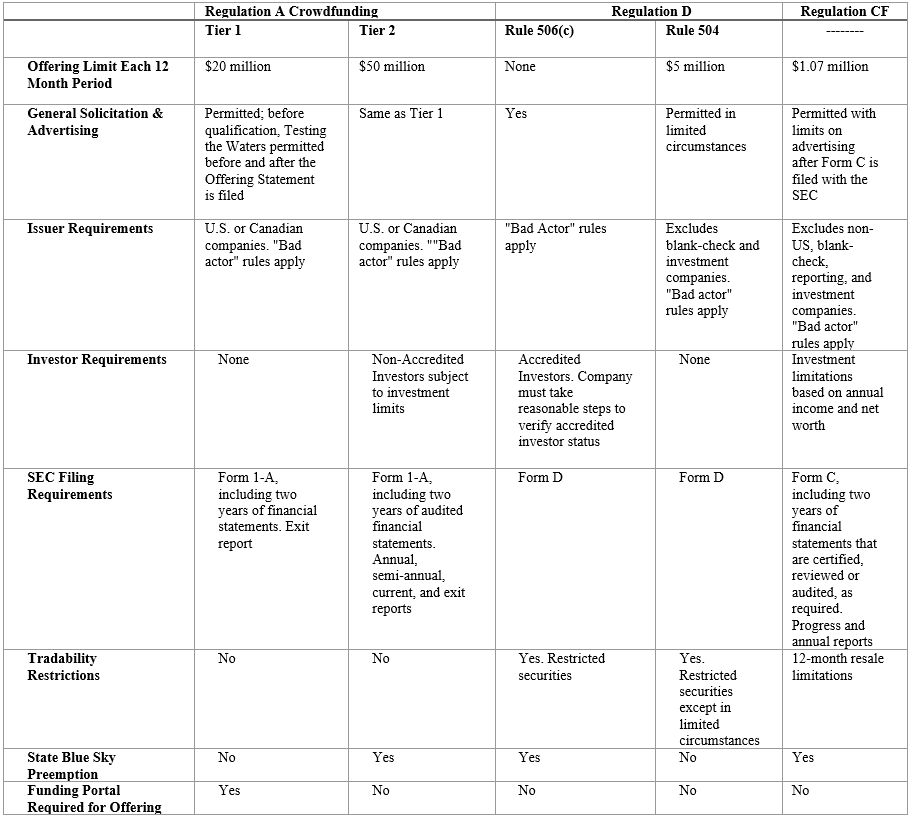

There are several securities exemptions available for crowdfunding offerings, each with unique benefits and requirements. Rules 504 and 506 of Regulation D do not require a filing with the SEC prior to raising funds, while Regulation Crowdfunding (“Regulation CF”) and Regulation A require an SEC review and qualification of the offering prior to sales.

- Regulation Crowdfunding (“Regulation CF”) offerings up to $1.07 million on offering portals registered with the SEC and FINRA.

- Regulation D, Rule 504 allows offerings of up to $5 million.

- Regulation D, Rule 506(c) allows you to raise an unlimited amount of capital from accredited investors using general solicitation and advertising as long as you take reasonable steps to verify sales are made to accredited investors only.

Choosing the Right Crowdfunding Exemption

Choosing the right crowdfunding exemption should be an informed decision. First of all, you need to consider how much money you want to try to raise. Some exemptions are capped at specific amounts. Base your choice on how much you realistically believe people will invest. Second, consider the kind of company you have. If it’s a development stage startup, for example, you may want to opt for a Regulation CF offering, which permits you to raise small sums from a large number of people. If it’s an operational company generating revenues and even profits, a Regulation D, Rule 506(c) offering, which allows you to raise an unlimited amount, might be the appropriate choice. Regardless of the crowdfunding exemption an issuer selects, it must disclose any material information to investors, whether specifically listed in the specific regulation or not. As the SEC says, material information must be provided as needed in order to render the statements made, in light of the circumstances under which they were made, not misleading. What’s material? It’s any information, positive or negative, that might persuade an investor to change his mind about an investment. If a company lands a new contract that will make a substantial difference to its bottom line, that’s material. If it finds it has an incompetent bookkeeper or auditor and needs to restate several years of financial statements, that’s material. The COVID-19 virus creates possible risks and uncertainties that aren’t the fault of any business owner. But if they’re material to the performance of the business, they must be disclosed in connection with any offering. We’ll explain more about this and other things a business owner considering raising money through a crowdfunding offering must take into account in the coming days and weeks.

Regardless of the crowdfunding exemption an issuer selects, it must disclose any material information to investors, whether specifically listed in the specific regulation or not. As the SEC says, material information must be provided as needed in order to render the statements made, in light of the circumstances under which they were made, not misleading. What’s material? It’s any information, positive or negative, that might persuade an investor to change his mind about an investment. If a company lands a new contract that will make a substantial difference to its bottom line, that’s material. If it finds it has an incompetent bookkeeper or auditor and needs to restate several years of financial statements, that’s material. The COVID-19 virus creates possible risks and uncertainties that aren’t the fault of any business owner. But if they’re material to the performance of the business, they must be disclosed in connection with any offering. We’ll explain more about this and other things a business owner considering raising money through a crowdfunding offering must take into account in the coming days and weeks.

Prior to conducting a crowdfunding offering, you should hire competent securities counsel to help you select the appropriate exemption and assist you with the SEC’s requirements including appropriate disclosures.

Hamilton & Associates Law Group, P.A. is providing guidance to help its clients identify and understand issues arising from COVID-19 Disclosure Requirements, address COVID-19’s potential effects on their businesses, and identify resources available to private and public companies that have been harmed by COVID-19. This securities law blog post is provided as a general informational service to clients and friends of Hamilton & Associates Law Group and should not be construed as, and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship.