Reverse Stock Splits by Nasdaq and NYSE Issuers

Public Companies whose securities are listed on the New York Stock Exchange (NYSE) and Nasdaq Stock Market (NASDAQ), particularly the NASDAQ Capital Market, frequently effect reverse stock splits to comply with NASDAQ and NYSE’s minimum $1.00 share price requirement.

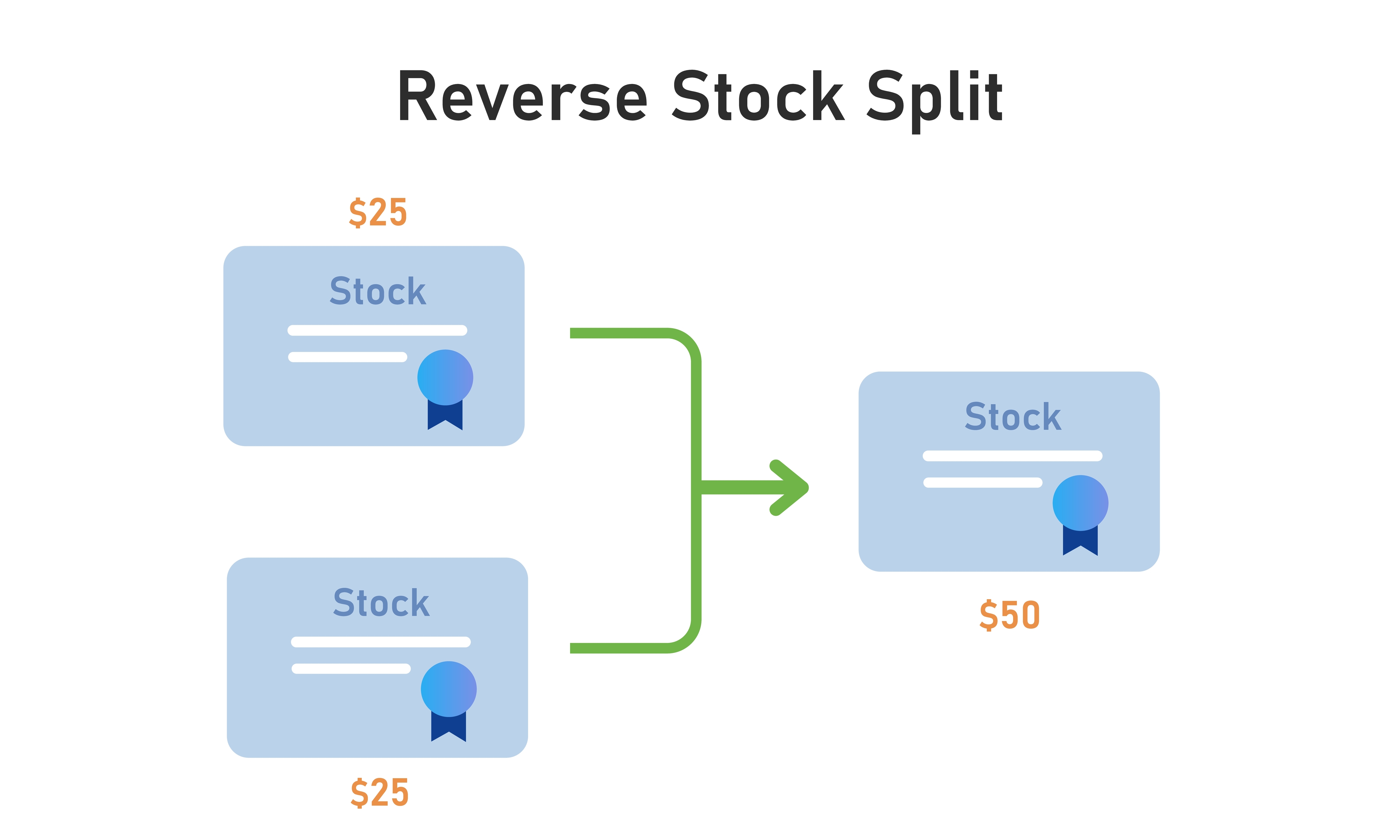

Reverse splits are neutral in theory. They only change the number of shares outstanding, not the value of shareholders’ positions in those shares. Therefore, they almost always increase the price of a public company’s securities by combining the issuer’s outstanding securities at a ratio so that after the reverse stock split, each stockholder maintains its approximate ownership percentage while the company has a lesser number of securities outstanding with a higher price per share.

However, it has become more common in recent years for exchange-listed companies (especially startups and biotechs) to enter into dilutive financings, where financiers receive securities in exchange for cash at a discount to the market price through convertible debt notes, convertible preferred stock, and warrants, which have a dilutive effect when converted/exercised, causing the company’s stock price to drop over time and leading to the company having to effect a reverse split to remain compliant with the listing standards. Oftentimes, companies involved in dilutive financings become repeat offenders, having to do two or more reverse splits to remain compliant with the listing standards. We’ve even witnessed some public companies effecting as many as four to five reverse stock splits in less than two years.

To address this issue, the NYSE and Nasdaq each proposed rule changes to limit a public company’s ability to enact a reverse stock split to regain compliance with the minimum share price requirement of $1.00 per share.

The US Securities and Exchange Commission (SEC) approved the NYSE’s proposed rule change on January 15, 2025. The rule change narrows options for NYSE-listed companies seeking to regain compliance with the $1.00 price criteria for common stock.

The SEC approved Nasdaq’s proposed rule change on January 17, 2025. The rule change accelerates the delisting process for companies with securities that fail to comply with the requirement to maintain a closing bid price above $1.00 per share.

New York Stock Exchange Rules

Under NYSE Section 802.01C, a public company is not in compliance with NYSE closing price requirements if the average closing price of its listed securities is less than $1.00 per share over a consecutive 30 trading-day period. The public company can regain compliance with NYSE requirements if, on the last trading day of any calendar month during a six-month cure period, the listed security has a closing price of at least $1.00 per share and an average closing share price of at least $1.00 during the prior 30 trading days. If an issuer attempts to cure the price deficiency by enacting a reverse stock split, it must obtain shareholder approval by no later than its next annual meeting of shareholders. The deficiency will be cured if the price of the issuer’s securities is above $1.00 for at least 30 trading days following the reverse stock split.

The newly approved amendment to NYSE Section 802.01C provides that a public company that fails to meet its trading price requirements is not eligible for any compliance period to cure the deficiency if (i) it has effected a reverse stock split over the past one-year period or (ii) has effected one or more reverse stock splits over the prior two-year period with a cumulative ratio of 200 shares or more to one. In such a case, the NYSE will instead immediately commence suspension and delisting procedures. Additionally, the amendment precludes issuers from conducting a reverse stock split if it would result in the company’s security falling out of compliance with any of the continued listing requirements of Section 802.01A of the Manual.

Nasdaq Stock Market Minimum Bid Price Rule

Nasdaq Stock Market companies must maintain a minimum bid price of $1.00. If the trading price closes under $1.00 per share for 30 consecutive business days, the company will generally have up to 180 days to regain compliance.

If at the end of the 180-day period, the public company has not regained compliance, it can request an additional 180-day compliance period by notifying Nasdaq of its intent to cure the trading price deficiency, including by enacting a reverse stock split.

The newly approved Nasdaq rule modifies the delisting process for securities that fail to regain compliance with the bid price requirement following the second 180-day compliance period and for securities that have had a reverse stock split over the prior one-year period.

Removal of Stay Period After Second 180-Day Compliance Period

Under the newly approved Nasdaq rule, Nasdaq will automatically suspend a company’s securities from trading on Nasdaq if the company has not regained compliance with the minimum $1.00 bid price requirement for a minimum of 10 consecutive business days prior to the end of the second 180-day period, even if it is appealing to a Nasdaq Listing Qualifications Hearings Panel.

While any appeal is pending, the securities will be quoted by the OTC Markets.

Penalties for NASDAQ Issuers Effecting Serial Reverse Splits

The newly approved Nasdaq rule also provides that a listed company will not be eligible for a compliance period to cure a deficiency under the minimum bid price requirement if it has effected a reverse stock split over the prior one-year period.

A listed company that receives a delisting determination under these circumstances can appeal for a hearing before a Nasdaq panel (during which time the suspension of trading of its securities will be stayed).

Conclusion

The newly approved rules will narrow the options for NYSE and Nasdaq-listed companies struggling to comply with the price criteria rule or bid price rule to remain listed on the NYSE or Nasdaq.

Before doing a reverse stock split, companies will have to think carefully about what ratio to choose and must consider their recent reverse stock split history over the past 2 years and the likelihood the company can remain in compliance with the price criteria rule or the bid price rule for a period of at least one year.

Companies will also have to consider carefully what financing options they choose because they could be sacrificing their ability to remain listed on the NYSE or Nasdaq.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected]. This securities law blog post is provided as a general informational service to clients and friends of Hamilton & Associates Law Group and should not be construed as and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship. Please note that the prior results discussed herein do not guarantee similar outcomes.

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com